Most mid-size companies have made real progress on SaaS spend visibility over the past few years. Some have extended that discipline to cloud infrastructure. Almost none have a structured approach to AI tool costs; by mid-2026, AI software subscriptions are the fastest-growing line in the technology budget at companies of every size.

The problem compounds when these three categories are managed separately. Different budget owners. Different renewal timelines. Different tools tracking each. No consolidated view of what the company is actually spending on technology, and no unified leverage to reduce it. The spend exists. The opportunity to optimize it exists. What is missing, in most cases, is structure.

This guide covers what it means to manage AI, SaaS, and cloud spend together: why AI tools are now a third distinct cost category, what the consequences of fragmented management look like in practice, and what a full-lifecycle optimization approach across all three categories actually covers.

Why AI Tools Are Now a Third Tech Spend Category

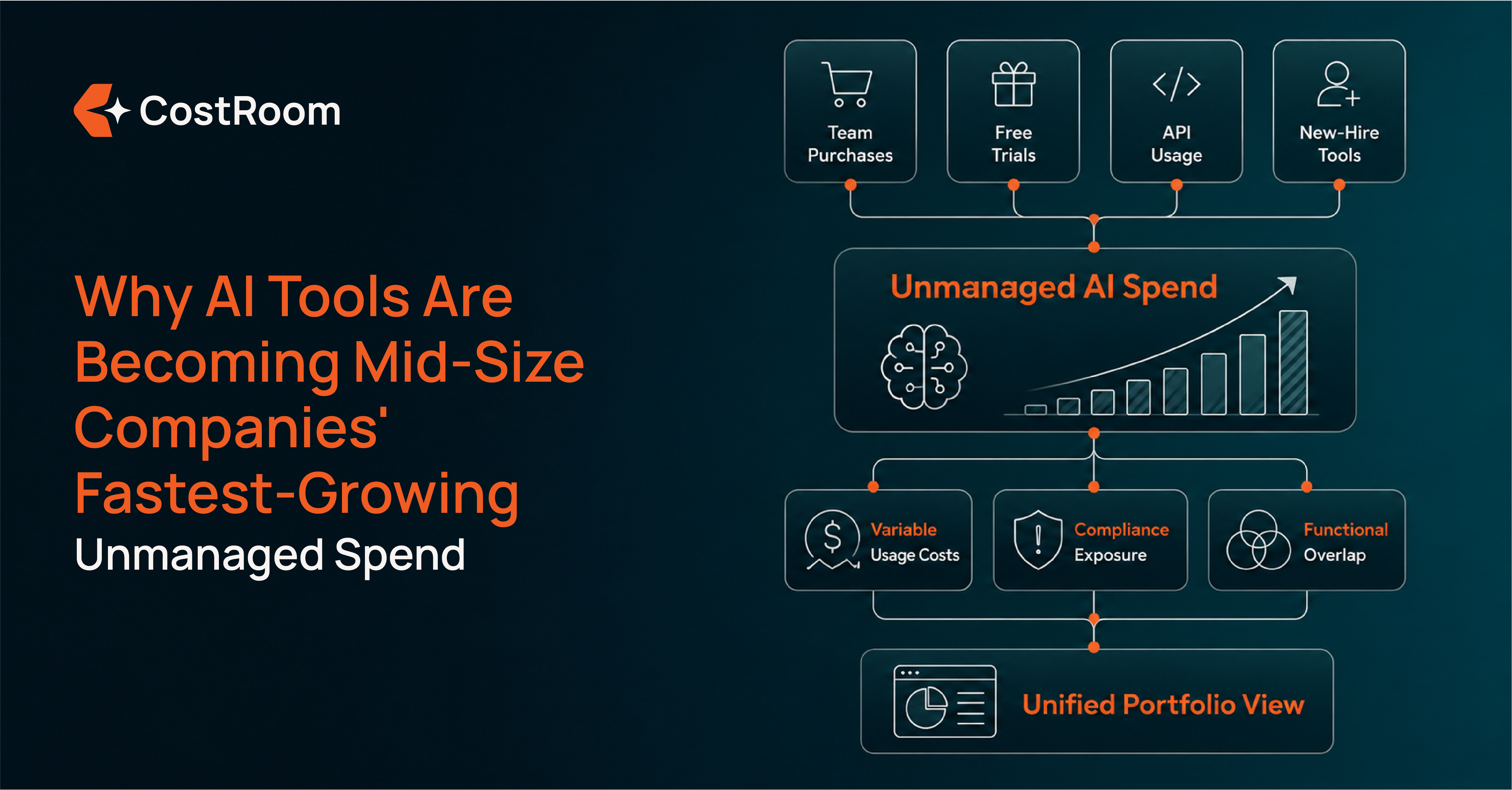

SaaS spend became a CFO priority when the number of tools per company crossed the point where individual budget owners could no longer track the total. That crossing point arrived at different times for different companies, but the pattern was consistent: tools entered through team purchases and free trial conversions, costs accumulated below any single approval threshold, and the total spend only became visible during a finance reconciliation or a CISO access review.

AI tools are following the same pattern, faster. ChatGPT Enterprise, Microsoft Copilot, vertical AI tools for specific business functions, model API keys being expensed by engineering teams as operational costs: by 2026, most mid-size companies are running multiple AI subscriptions simultaneously, and few have mapped the total cost.

Three factors make AI spend harder to manage than SaaS spend was at the equivalent stage. First, pricing models are more variable. API-based AI tools charge by token or by usage volume, which means costs can increase materially within a contract period without any renewal event triggering a review. A model API key in heavy use by an engineering team can double its monthly cost without any contract change. Second, the data handling considerations are more acute. AI tools often process more sensitive data than equivalent SaaS tools: customer data, internal communications, financial records. This means an unreviewed AI tool carries both the financial exposure of uncontracted spend and a compliance exposure that is often larger than the equivalent SaaS tool. Third, overlap is harder to detect. Two AI tools performing similar functions frequently look entirely different at the surface, which makes consolidation decisions harder without a structured portfolio view.

The implication is that managing SaaS and cloud spend without also managing AI spend produces an incomplete picture, and the gap is growing. For more on how uncontracted tools accumulate and what the full cost looks like, see Why AI Tools Are Becoming Mid-Size Companies' Fastest-Growing Unmanaged Spend.

What Happens When You Manage Three Categories Separately

Fragmented management of SaaS, cloud, and AI spend produces three specific and predictable failures.

The first is an incomplete picture at the CFO level. When tech spend is tracked by category: SaaS budget here, cloud infrastructure budget there, AI subscriptions scattered across operational expense accounts. The total is never visible in one place. Finance knows the approximate figures for each budget line. IT knows something about usage. Procurement has contracts for the tools that went through a formal process. Nobody has the full picture, because the full picture requires consolidating data from three separate processes that were not designed to talk to each other.

The second failure is misaligned renewal timing. SaaS, cloud, and AI tools rarely renew on coordinated schedules. When renewal attention is concentrated on one category at a time, the leverage windows in the other two categories close unnoticed. A company spending heavily on AWS committed spend, Microsoft 365 seats, and an expanding set of AI subscriptions has three distinct renewal cycles, each representing real cost reduction opportunity. Managing them separately means those opportunities are sequenced rather than coordinated, and the leverage that comes from presenting a complete portfolio view to a vendor is never used.

The third failure is fragmented vendor relationships. Many mid-size companies have commercial relationships with the same vendors across multiple categories: Microsoft for cloud infrastructure, Microsoft 365 for SaaS productivity, and Microsoft Copilot for AI functionality. Managing those relationships through three separate processes, cloud commitment renewals through IT, SaaS renewals through procurement, AI subscriptions through whoever owns the budget, means the aggregate relationship with that vendor is never brought to bear on any individual negotiation. The leverage that comes from portfolio-level relationships is left unused.

What Full Lifecycle Optimization Covers Across All Three Categories

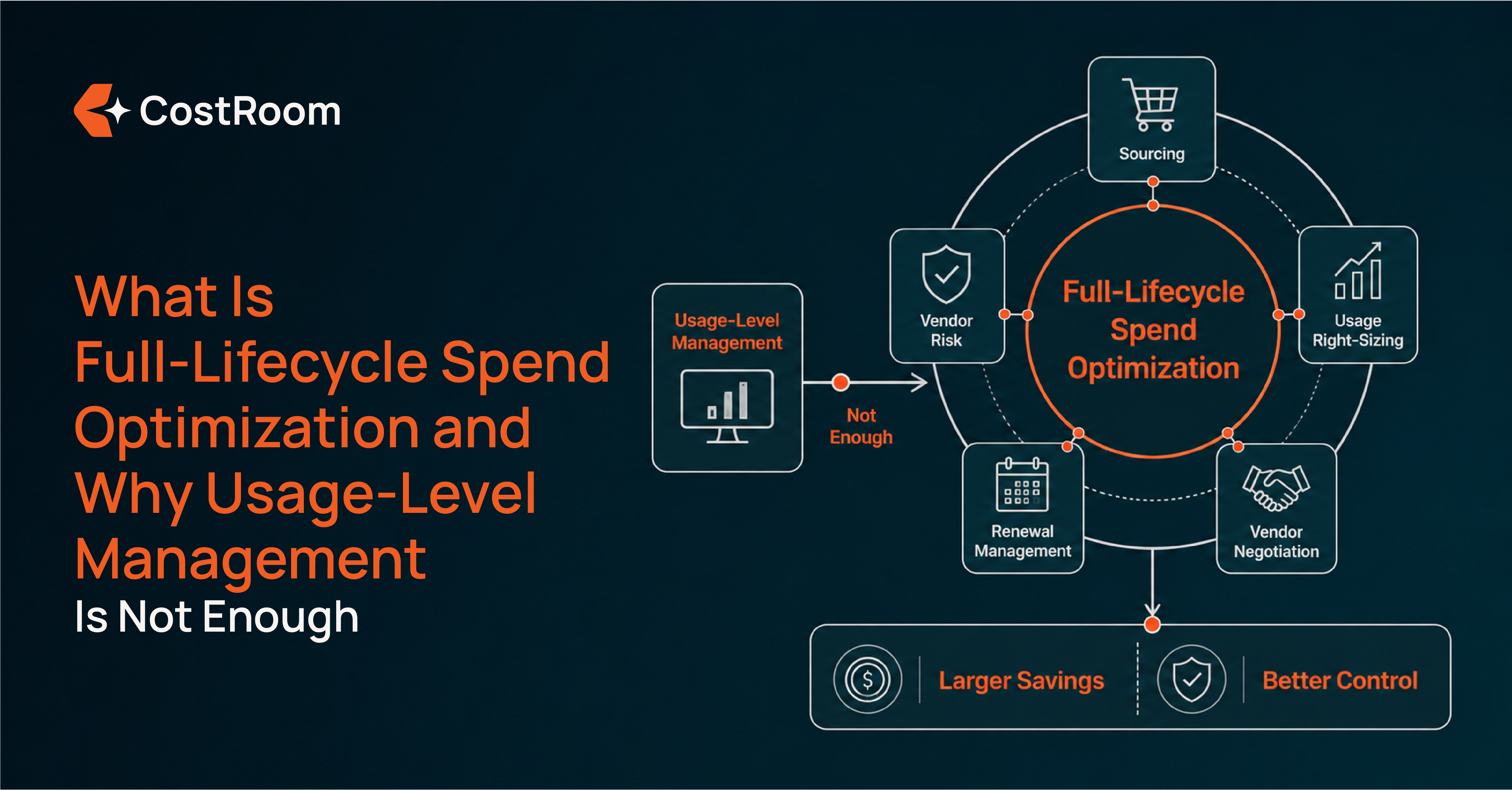

Lifecycle optimization across SaaS, cloud, and AI spend covers five layers. Most tools and most internal optimization efforts address one or two of these layers. Addressing all five, across all three spend categories, is what full lifecycle optimization means in practice.

Sourcing. The first layer, and the one most optimization approaches skip. The entry price for a new tool, specifically the price negotiated at the moment the first contract is signed, sets the baseline for every future renegotiation. Companies that source at list price because no benchmarking was done before signing are negotiating every subsequent renewal against an above-market starting point. Sourcing optimization means entering contracts at structured rates, using market intelligence and established vendor relationships rather than list price as the starting point. This applies equally to SaaS tools, cloud commitments, and AI subscriptions.

Usage right-sizing. The layer most companies do address, at least partially. Licence counts aligned to actual usage, cloud committed spend aligned to actual consumption, AI subscription tiers aligned to actual workload requirements. This is necessary work. It is not sufficient on its own, because right-sizing at a price that was never benchmarked still leaves the company paying more than it needs to.

Vendor negotiation. Bringing market benchmarks and renewal leverage to bear on vendor pricing across the portfolio. For SaaS and AI tools, this means knowing what comparable companies at the same size and volume pay and using that data in renewal conversations. For cloud, this means optimizing committed spend structures, reserved instance coverage, and enterprise agreement terms. Negotiation without benchmarking is guesswork. Benchmarking without negotiation is analysis without action.

Renewal management. Tracking renewal dates and notice periods across the full portfolio, covering SaaS, cloud, and AI, so that no tool auto-renews without review. The 90-day window before renewal is when leverage exists. After the renewal executes, the terms are locked for another year. A structured renewal calendar that covers all three categories closes the window in which costs can compound without anyone reviewing them. For a detailed guide on how renewal management works, see SaaS and Cloud Contract Renewal Management: The Complete Guide.

Vendor risk. Mapping financial, compliance, security, and concentration risk across the full portfolio. For AI tools specifically, the compliance dimension has grown significantly: tools processing customer or employee data under AI models carry data handling requirements that are more stringent in many markets than equivalent SaaS tools. A vendor risk assessment that covers SaaS and cloud but not AI produces a partial risk picture. For the full framework covering vendor risk across the portfolio, see SaaS and Cloud Vendor Risk Management: The Complete Guide.

For a deeper explanation of what lifecycle optimization covers and how it differs from usage-level management, see What Is Full-Lifecycle Spend Optimization and Why Usage-Level Management Is Not Enough.

See Your Full Tech Spend in One View

CostRoom maps SaaS, Cloud, and AI spend together, then optimises across every layer from sourcing to renewal.

How the Vendor Sourcing Network Changes What's Possible

Sourcing is the layer of optimization that requires something a software tool cannot provide: established vendor relationships and live market intelligence across a large number of vendors simultaneously.

CostRoom's sourcing network covers more than 100 SaaS, Cloud, and AI vendors, and that number is growing as the AI vendor landscape expands. The network carries no OEM agreements and no commercial relationships with vendors. CostRoom does not earn from vendor referrals, holds no exclusivity arrangements, and recommends tools based only on client data and market fit. This vendor-agnostic position means the sourcing recommendation reflects what the data shows, not what any commercial relationship incentivises.

What this changes in practice: clients sourcing new tools through CostRoom's network access structured pricing rather than list price, based on existing vendor relationships and current market rate data. For AI tools specifically, a category where published pricing is rarely what informed buyers pay, this means entering a contract at a price that reflects actual market conditions rather than the vendor's preferred starting point.

The sourcing benefit compounds across the lifecycle. A tool sourced at the right price, with a well-structured initial contract, is easier to renegotiate at renewal and carries a lower baseline that every subsequent negotiation builds from. Companies that optimize only at the renewal stage are correcting, at each cycle, a pricing problem that sourcing discipline would have prevented at the start. For a detailed guide on how the vendor sourcing network works and what it changes about entry pricing, see How a Vendor Sourcing Network Gives Mid-Size Companies Buying Power They Don't Have Alone.

One Platform for SaaS, Cloud, and AI Spend

Managing three categories of spend across three separate systems produces three incomplete pictures. Finance tracks invoices. IT tracks access and usage. Procurement tracks contracts, specifically for the tools that went through a formal procurement process. None of these views, individually or in combination, produces the consolidated portfolio view a CFO needs: total tech spend, total optimization opportunity, sequenced by renewal urgency and savings potential.

CostRoom's unified platform covers SaaS, Cloud, and AI spend together. One view of every active tool, subscription, and cloud commitment across all three categories. Renewal dates tracked across all three. Vendor benchmarks applied across all three. Risk assessment across all three. The optimization work that follows, covering renegotiating contracts, right-sizing usage, managing renewals, and addressing compliance gaps, is more effective when it is coordinated across the full portfolio than when it is run category by category, because the leverage from the complete relationship with any vendor only exists when the complete relationship is visible.

This is the structural difference between managing tech spend as three categories and managing it as one optimization discipline. The spend is the same. The leverage is materially different. For context on how spend visibility across the full SaaS and cloud portfolio works, see SaaS and Cloud Spend Optimization: The Complete Guide for Mid-Size Companies.

Getting Started: The Spend Analysis

The starting point for managing AI, SaaS, and cloud spend together is a complete, current picture of what the company is actually spending across all three categories: contracted and uncontracted, usage-tracked and untracked, renewal dates mapped and unknown.

CostRoom's spend analysis covers the full portfolio before any optimization work begins. Every SaaS tool, every cloud commitment, every AI subscription: current cost, renewal date, contract status, pricing relative to current market benchmarks, and risk flags for compliance and concentration exposure. The output is a prioritised action plan: which renewals to address in the next 90 days, which tools to renegotiate, which AI subscriptions to consolidate or exit, which compliance gaps need attention before the next regulatory inquiry arrives.

The spend analysis is not a report that gets filed. It is the working document from which the negotiation calendar, the renewal management schedule, the right-sizing programme, and the risk remediation plan are all built. Most companies completing this analysis for the first time find two things simultaneously: their tech spend total is higher than any budget estimate, and the optimization opportunity across all three categories is larger than any single-category effort would have surfaced.

Managing AI, SaaS, and cloud spend together is not a new discipline. It is the logical extension of the spend optimization work that mid-size companies have been doing for SaaS and cloud, applied to a third category that has arrived faster and carries more complexity than either of its predecessors. The companies that establish a unified approach now, sourcing at structured rates, right-sizing usage, managing renewals, negotiating with benchmarks, and assessing risk across the full portfolio, will not be relearning this process in two years for the next category of spend that arrives.

Frequently Asked Questions

What does it mean to manage AI, SaaS, and cloud spend together? Managing AI, SaaS, and cloud spend together means treating all three as a single technology spend portfolio, with a unified view of every tool and subscription, a coordinated renewal management process, shared benchmarking data for vendor negotiations, and a single risk assessment framework covering compliance and concentration across all three categories. The alternative is managing three separate processes with three incomplete pictures, which leaves leverage unused in each category because the portfolio-level relationship with each vendor is never visible.

Why are AI tools now a third tech spend category? AI tools have entered company budgets through the same channels as SaaS: team adoption below procurement thresholds, free trial conversions, and rapid growth phases where procurement processes have not kept up with adoption pace. By 2026, most mid-size companies are running multiple AI subscriptions simultaneously, many of them uncontracted or unreviewed. AI tools add specific complexities SaaS did not: variable API-based pricing that can increase within a contract period, more acute data handling compliance requirements, and functional overlap that is harder to detect than in most SaaS categories.

What is full lifecycle spend optimization? Full lifecycle spend optimization covers five layers of a vendor relationship: sourcing (entry pricing and initial contract structure), usage right-sizing (aligning licences and resources to actual consumption), vendor negotiation (benchmarking and renegotiation using market data), renewal management (tracking renewal dates and notice periods to prevent unreviewed auto-renewals), and vendor risk (financial, compliance, security, and concentration risk assessment). Most tools and most internal efforts address one or two of these layers. Addressing all five, across SaaS, Cloud, and AI, from a single platform, produces consistently larger savings than any single-layer approach.

How does a vendor sourcing network help mid-size companies reduce tech costs? A vendor sourcing network provides access to structured pricing and market intelligence at the sourcing stage, before a contract is signed. This matters because the entry price sets the baseline for every future negotiation: a company that sources at list price is negotiating every subsequent renewal against an above-market starting point. CostRoom's sourcing network of 100+ SaaS, Cloud, and AI vendors operates with no OEM agreements and no commercial vendor relationships. The benefit flows entirely to the client, in the form of structured entry pricing and live market rate data.

What is the difference between a unified platform and managing spend by category? A unified platform that covers SaaS, Cloud, and AI spend together produces a consolidated portfolio view: total tech spend, total optimization opportunity, renewal calendar across all three categories, and the full picture of the company's relationship with each vendor. Managing spend by category produces three separate pictures, each accurate within its category and incomplete at the portfolio level. The leverage available to a company that presents its full relationship with a vendor is materially greater than the leverage available to one that negotiates each category independently.

Why does the entry price matter more than the renewal rate? Every vendor negotiation starts from the existing contract as a baseline. A company that first contracted a tool at list price, because no benchmarking was done before signing, is negotiating every future renewal against an above-market starting point. Even a successful 10% reduction at renewal may still leave the company above where a well-sourced initial contract would have started. Sourcing optimization, which sets the correct entry price based on market data and established vendor relationships, removes this structural disadvantage before it compounds across multiple renewal cycles.

Start With a Full Spend Analysis

CostRoom maps SaaS, Cloud, and AI spend together before any optimization work begins.